National Property Market Report: August 2022

Key statistics

Summer Sense

The race to be the UK’s next Prime Minister is hotting up, while there are signs that the economic pressures are starting to impact the housing market. With the economy a key battleground, is Rishi Sunak or Liz Truss set to enter the door of Number 10 in just a month’s time, and where will housing feature in the forthcoming political agenda?

Economic Election

After a turbulent month in British politics the race is on to find the UK’s next Prime Minister. As inflation continues to edge upwards, public sector pay negotiations make the headlines and the war in Ukraine continues, the economic response of the UK’s next Prime Minister matters.

Although the UK economy grew by 0.5% in the year to May, now estimated to be 1.7% above its pre-pandemic level (ONS), the IMF report the global economy has shrunk for the first time since 2020. In response it has downgraded expectations for economic growth in 2023, predicting UK growth of just 0.5%, far lower than its 1.2% forecast in April. UK inflation, currently at 9.4% in the year to June and at its highest rate since 1982, is not expected to revert to the government’s 2% target for two years.

The Bank of England raised interest rates on August 4th by 0.5%, taking the base rate to 1.75%, its highest level since December 2008. In a clear sign the current situation is a global economic issue, the Eurozone raised interest rates for the first time in a decade in mid-July, while the United States Federal Reserve raised its target benchmark interest rate to between 2.25% and 2.5% after two consecutive 0.75% rises in June and July.

Reducing Speed

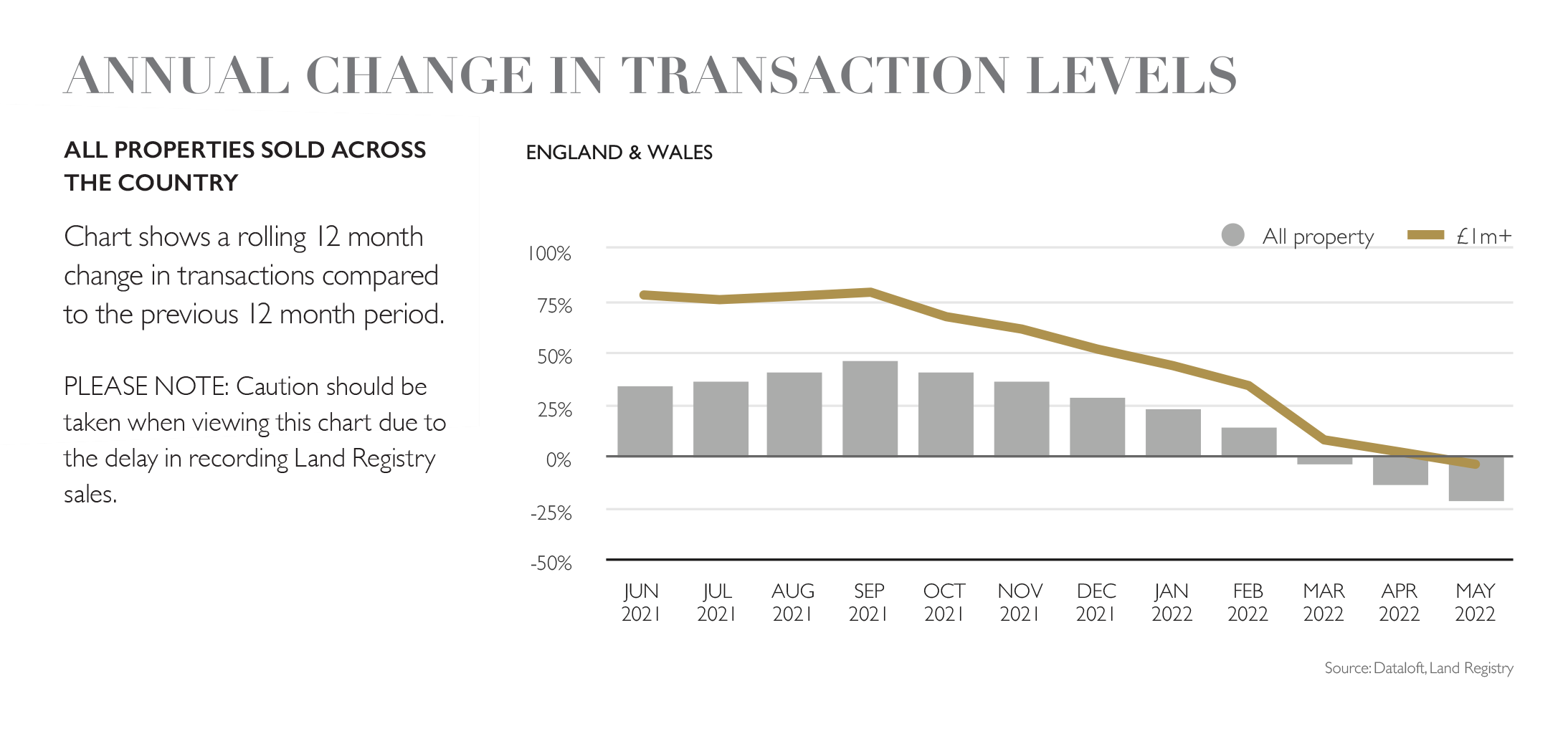

Property prices continue to rise across England and Wales, with low levels of stock continuing to underpin prices. Buyer demand continues to run above pre-pandemic levels, but levels of new buyer enquiries are starting to ease. RICS report that the net balance of agents predicting price growth over the next three and twelve months, while still positive across all regions of the UK, has pared back from the levels witnessed at the start of the year. At 95,420 the estimate for sales volumes in June is 8% lower than in May, and 6% lower than the pre-pandemic (2015–2019) average. HMRC

data indicates this is the first time in 2022 that volumes have dipped beneath 100,000. Considered a barometer for future market activity, mortgage approvals also fell below their prepandemic average in June. 63,726 mortgages were approved in June, the lowest monthly total since the COVID-19 market shutdown (Bank of England). Lending however remains high with remortgage activity in 2022 tracking above average. At present many buyers remain resolute on price, less than half of properties listed for sale for more than ten weeks having been reduced in price (Homesearch).

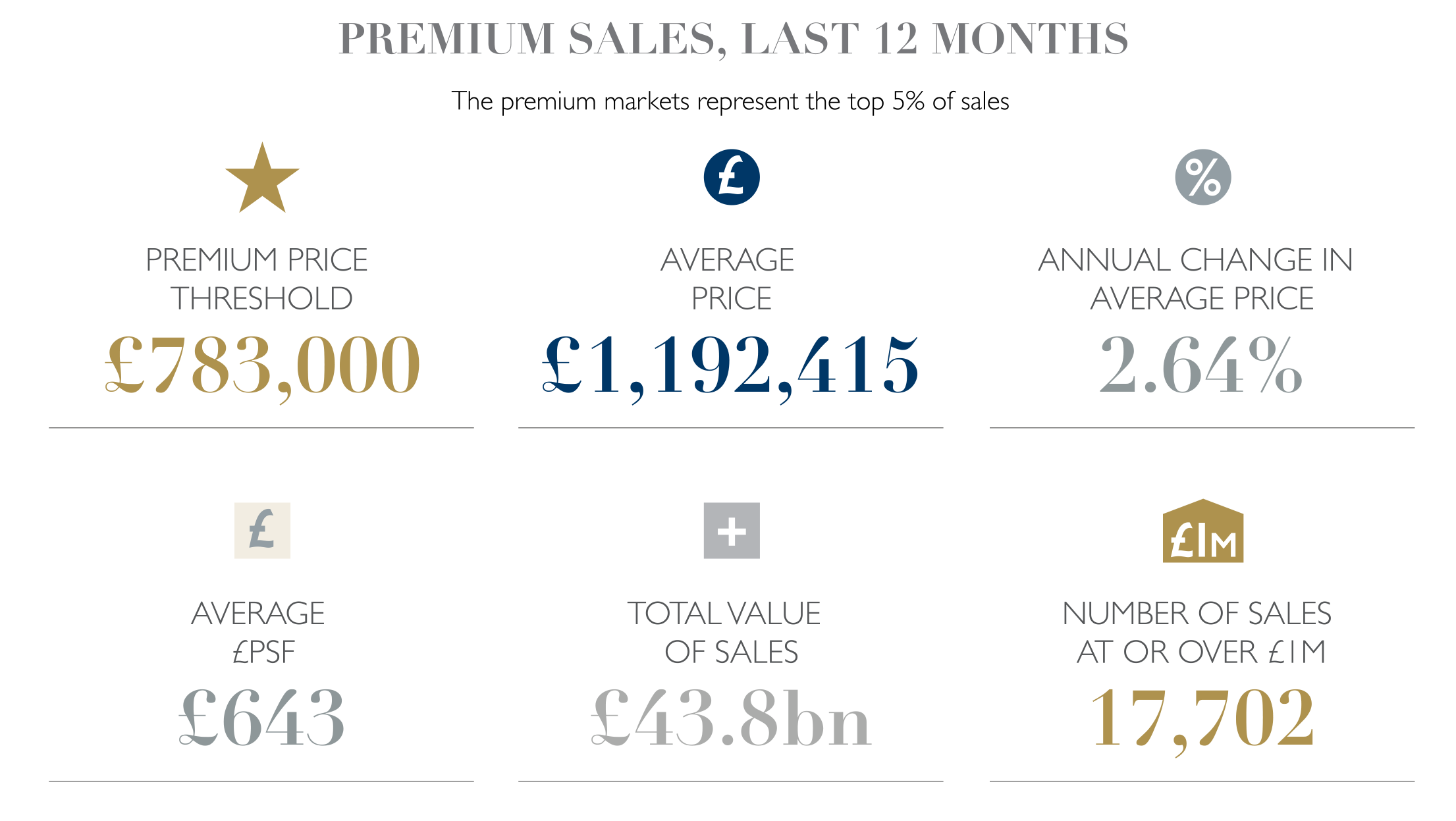

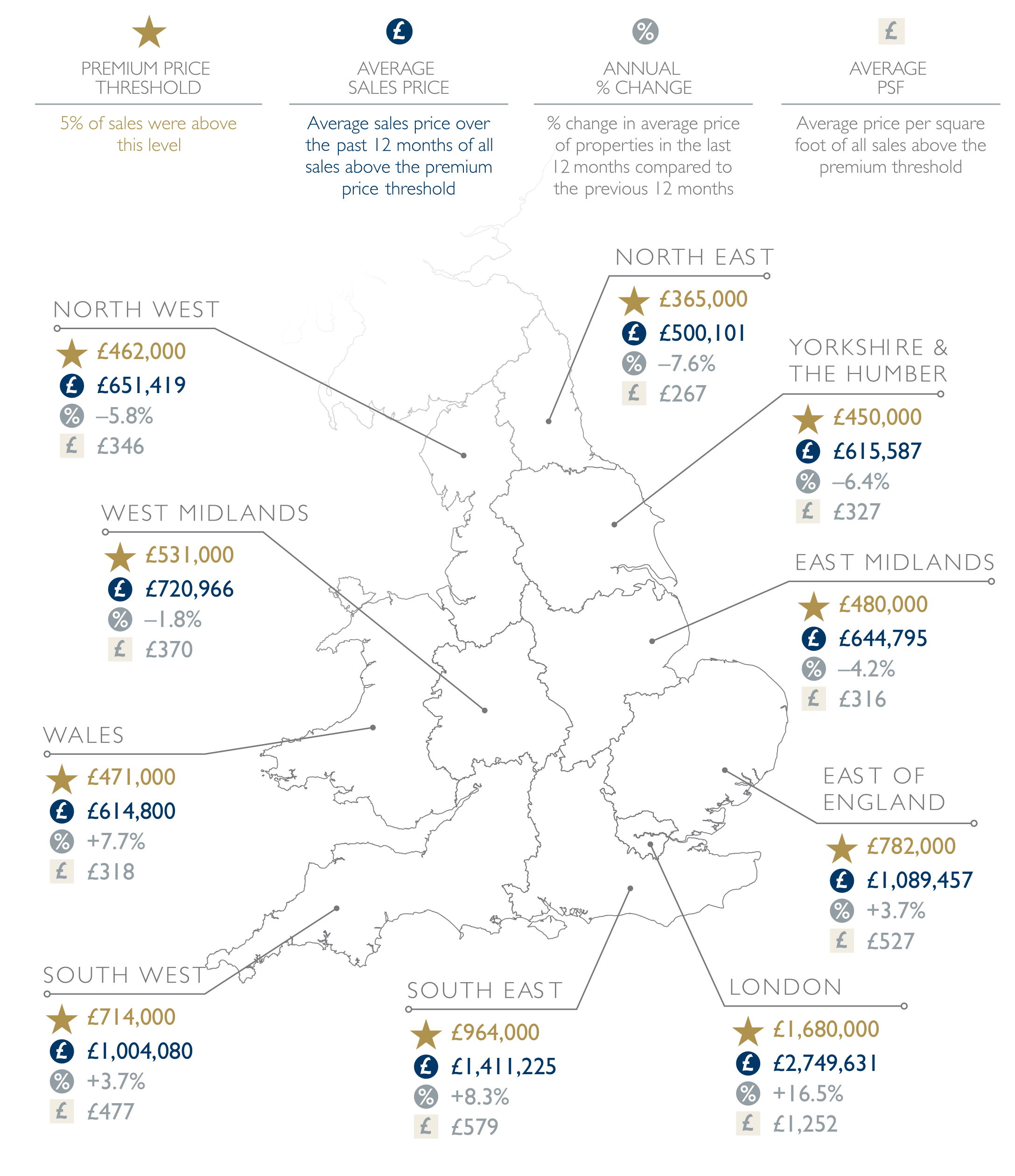

Prime Markets

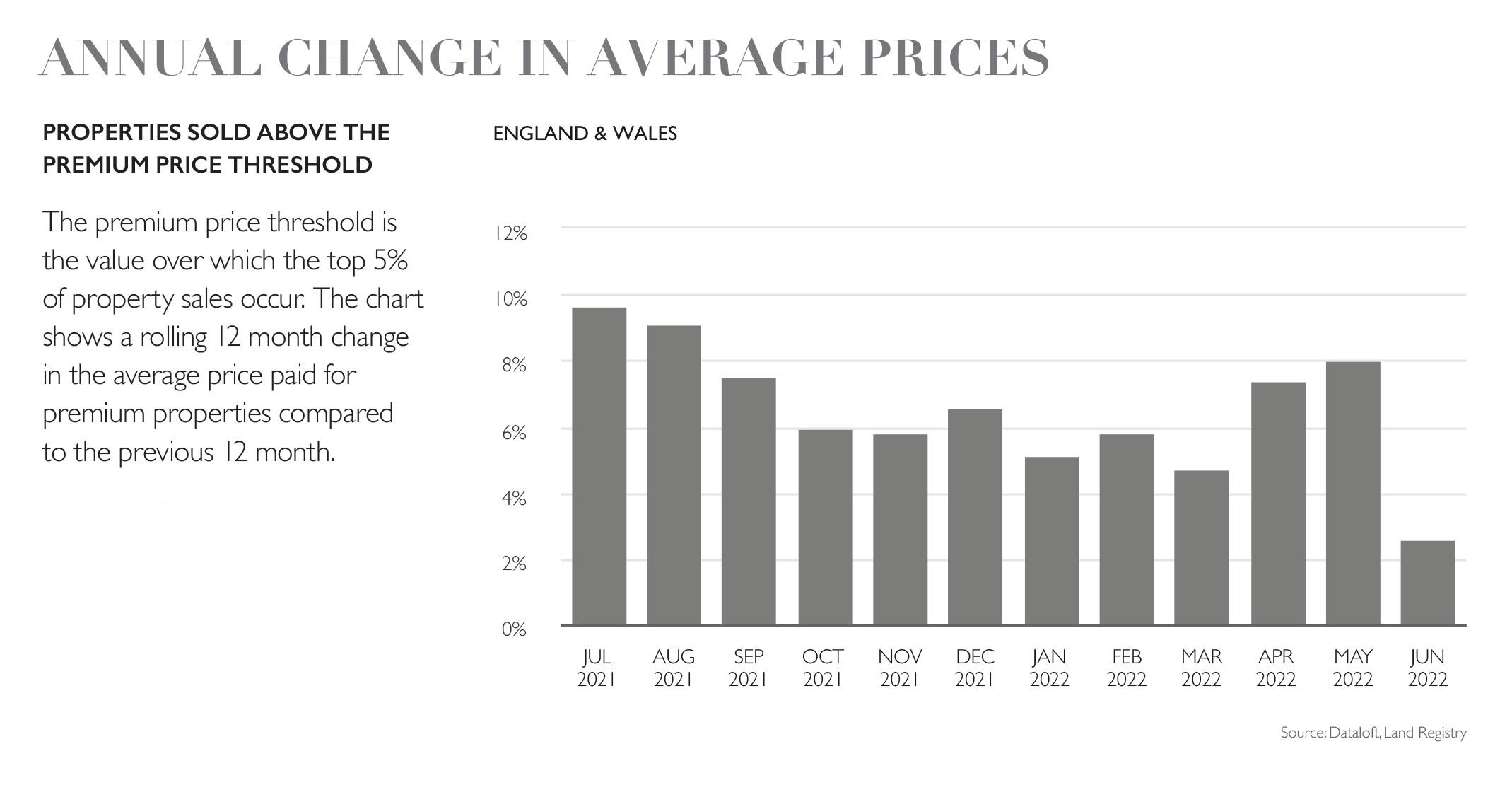

The prime markets across England and Wales continue to perform well across many regions of England and Wales. The price threshold for a premium property now stands at £783,000 while the average price of a prime market property, at close to £1.2 million is 2.6% higher than a year ago. More than one in three agents report that sales prices are coming in above asking prices for properties marketed at between £500k and £1 million. Higher levels of negotiations are taking place on properties listed at more than £1 million (RICS). The prime markets of London and the South East are currently seeing the strongest levels of price growth of all markets across England and Wales.

Contact us

Market your home this August with your prime property partner. Get in touch with your local Fine & Country agent to sell your home today.

9th Aug 2022

More from Fine & Country

DISCOVER MORE ABOUT FINE & COUNTRY

NATIONAL MARKET REPORTS

Looking at selling, buying, investing or just interested in the prime property market? Read our latest edition of the National Housing Market Update.

Discover more »

SELLING YOUR PROPERTY

Selling your home is one of the most important decisions you make; your home is both a financial and emotional investment. Find out how we can help »

TAKE THEIR WORD FOR IT

An overwhelming majority of those who had used Fine & Country would recommend our services to a family member or friend, according to our most recent survey taken by members of the public.

To achieve 99.48% positive feedback is a privilege and we will endeavour to maintain this result. We are dedicated to offering the best possible services to every customer, whether buyer or seller, from beginning to end.

INDEPENDENT EXPERTISE

Every Fine & Country agent is a highly proficient and professional independent estate agent, operating to strict codes of conduct and dedicated to you. They will assist, advise and inform you through each stage of the property transaction.

GLOBAL EXPOSURE

With offices in over 300 locations worldwide we combine the widespread exposure of the international marketplace with national marketing campaigns and local expertise and knowledge of carefully selected independent property professionals.

UNIQUE MARKETING APPROACH

People buy as much into lifestyle of a property and its location as they do the bricks and mortar. We utilize sophisticated, intelligent and creative marketing that provides the type of information buyers would never normally see with other agents.

PARK LANE OFFICE

Access the lucrative London and international investor market from our prestigious Park Lane showrooms at 121 Park Lane, Mayfair. Our showrooms in London are amongst the very best placed in Europe, attracting clients from all over the world.

MULTI-AWARD WINNING

Our consistent efforts to offer innovative marketing combined with a high level of service have been recognised by the industry for an astounding fifth year in a row, winning Best International Real Estate Agency Marketing at the International Residential Property Awards.

4.85 out of 5 - based on 1983 customer reviews

OVER 300 LOCATIONS WORLDWIDE

Our International Network

Connecting offices on over 300 locations worldwide, our referral system combines local knowledge and expertise with an international network to find the right buyer for you wherever they are, at the same time as finding you your ideal next move

Our International Websites

SOCIAL MEDIA

We interact with customers on the main social media channels including Facebook, Twitter, YouTube, LinkedIn and Pinterest, giving each property maximum online exposure.

FINE & COUNTRY SERVICES

FINE & COUNTRY

INTERIOR DESIGN

Access Fine & Country Interior Design to put your property ahead and make it stand out. With expert advice from some of London’s best stylists and designers we will make sure it makes a statement. Or if you’re purchasing with us, let F&C ID help make your new house feel like home by helping you find the very best specialists and designers for property refurbishment. Find out more »

FINE & COUNTRY

FOREIGN EXCHANGE

We have partnered with Rational FX, one of the world’s leading foreign exchange specialists to provide private and tailored currency services for all of our clients buying and selling luxury property around the world. Find out how we can help »

BUYING AGENT SERVICE

We understand that your time is precious, so save the time, money and stress of searching for a property with a buying agent. Also giving you access to off-market and discreetly marketed properties.

MEDIA CENTRE

Our internal Media Centre is a team of experienced press relations managers and copy writers dedicated to liaising with newspapers, magazines and other media outlets to gain extensive coverage for our properties in national and local media.

FINE & COUNTRY PUBLICATIONS

{kind=link}

THE FINE & COUNTRY FOUNDATION

The Fine & Country Foundation is dedicated to supporting and funding homeless causes in the UK and overseas. Fine & Country offices organise a range of fundraising events for you to get involved in and/ or support. Find out more about our work here. Read more »

*Please, note: for security reasons, the maps on this website do not provide the exact location of the property and they are provided solely as an indication of area.