National Property Market Report: June 2022

Key statistics

Now and then

Across all areas of the UK demand for property continues to outpace available supply, with asking prices hitting new record highs for the third month in succession. However, the housing market is undoubtedly set to reach a crossroads in the coming months as household budgets face increased pressure and economic headwinds escalate.

70 years’ service

The UK’s longest-running house price index, produced by the Nationwide, commenced in the same year the Queen ascended to the throne. At that time the average price of a property was just shy of £2,000; adjusting for inflation that’s the equivalent of around £60,000 today. All the national house price indices agree that the average price of a UK property is now more than £250,000. Back then the base rate of interest was 4%; today it’s just 1%, although the cost of home ownership compared to average earnings has increased significantly. The 1951 Census indicates there were just over 13 million households in England and Wales, with most of the population (65%) living in private rented accommodation. Today the figures have flipped: 65% of the estimated 26 million households in England and Wales are owner occupiers. The official 2021 Census household figures will be released by the Office for National Statistics later this month.

A chink in the armour

Month-on-month and year-on-year price growth continues. However, although Nationwide report prices rose 11.2% in the year to May, the 10th consecutive month of price growth, year-on-year this represents a slight slowdown from the 12.1% recorded in the year to April. Since mid-April, Zoopla report there has been a slight uptick in properties selling with a price reduction of 5% of more. The time taken to sell a property has edged upwards from 16 days in March to 18 days in April (Zoopla).

Mortgage approvals, an indicator of future borrowing and thus a good lead indicator of housing market activity, also dipped in April. The Bank of England report 66,000 mortgages were approved, a 5% fall on March and marginally lower than the pre-pandemic April average (2016-2019). The effective interest rate, the actual interest rate paid on newly-drawn mortgages, increased by 9 base points to 1.82%, and the rate on outstanding mortgages increased to 2.05%. With the additional rise in the base rate to 1% in May yet to filter through, it is likely these will creep upwards in future months. However, the average mortgage rate on fixed-rate 2- and 5-year 95% loan-to-value (LTV) deals remains lower than a year ago and any market moderation is anticipated to be gradual. A consensus of forecasts still predicts price growth of more than 5% across the mainstream markets over the course of 2022.

Crunching the numbers

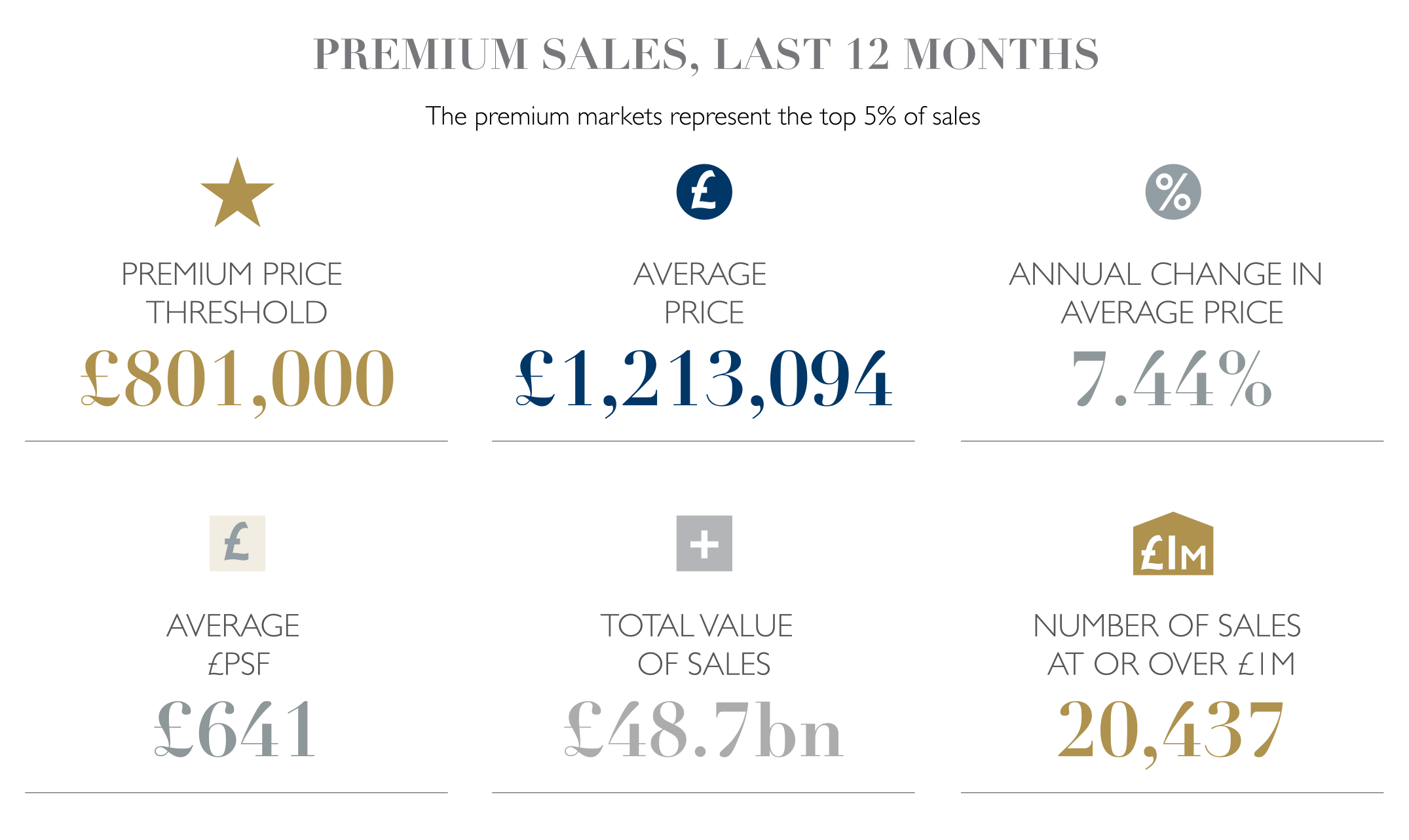

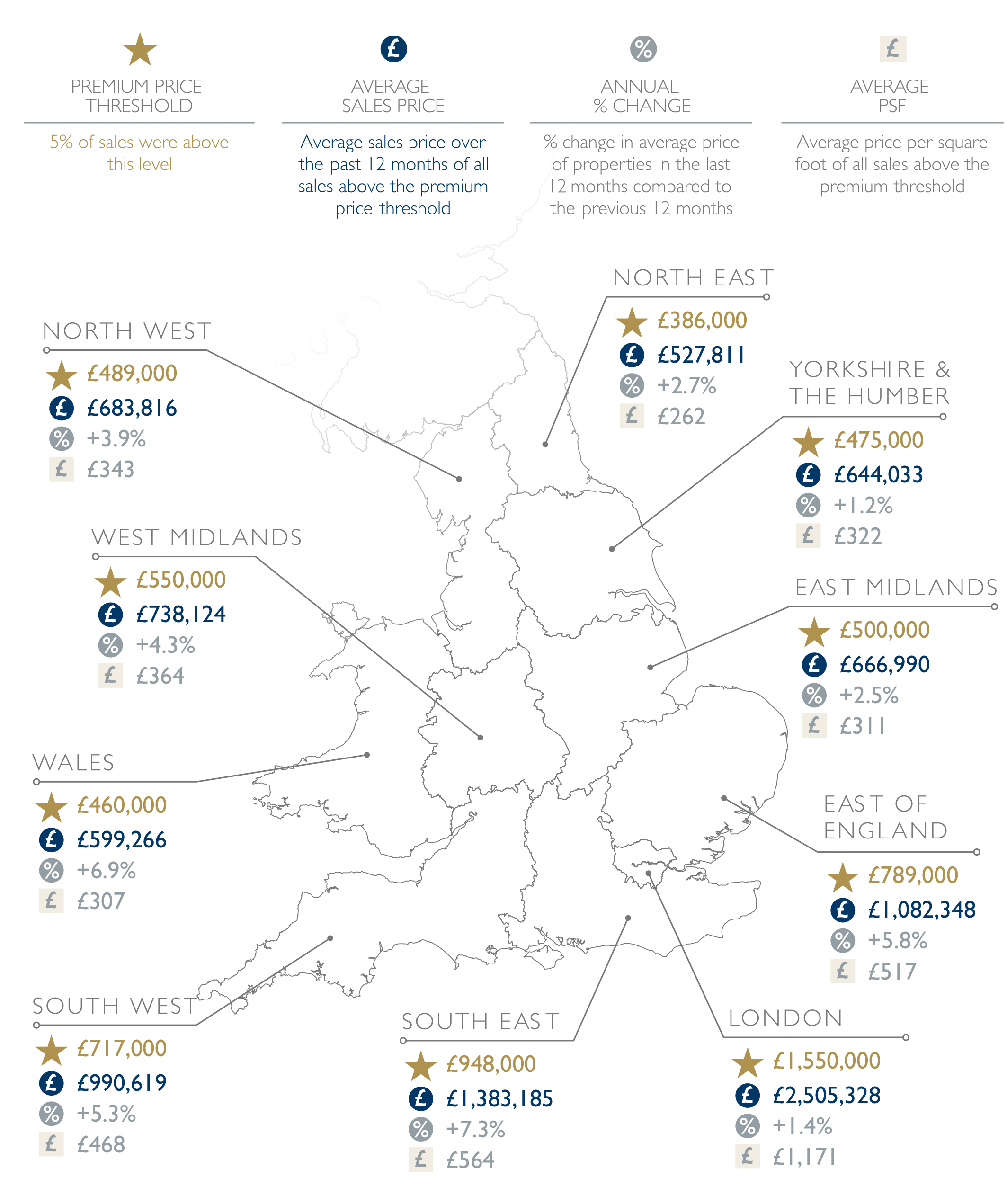

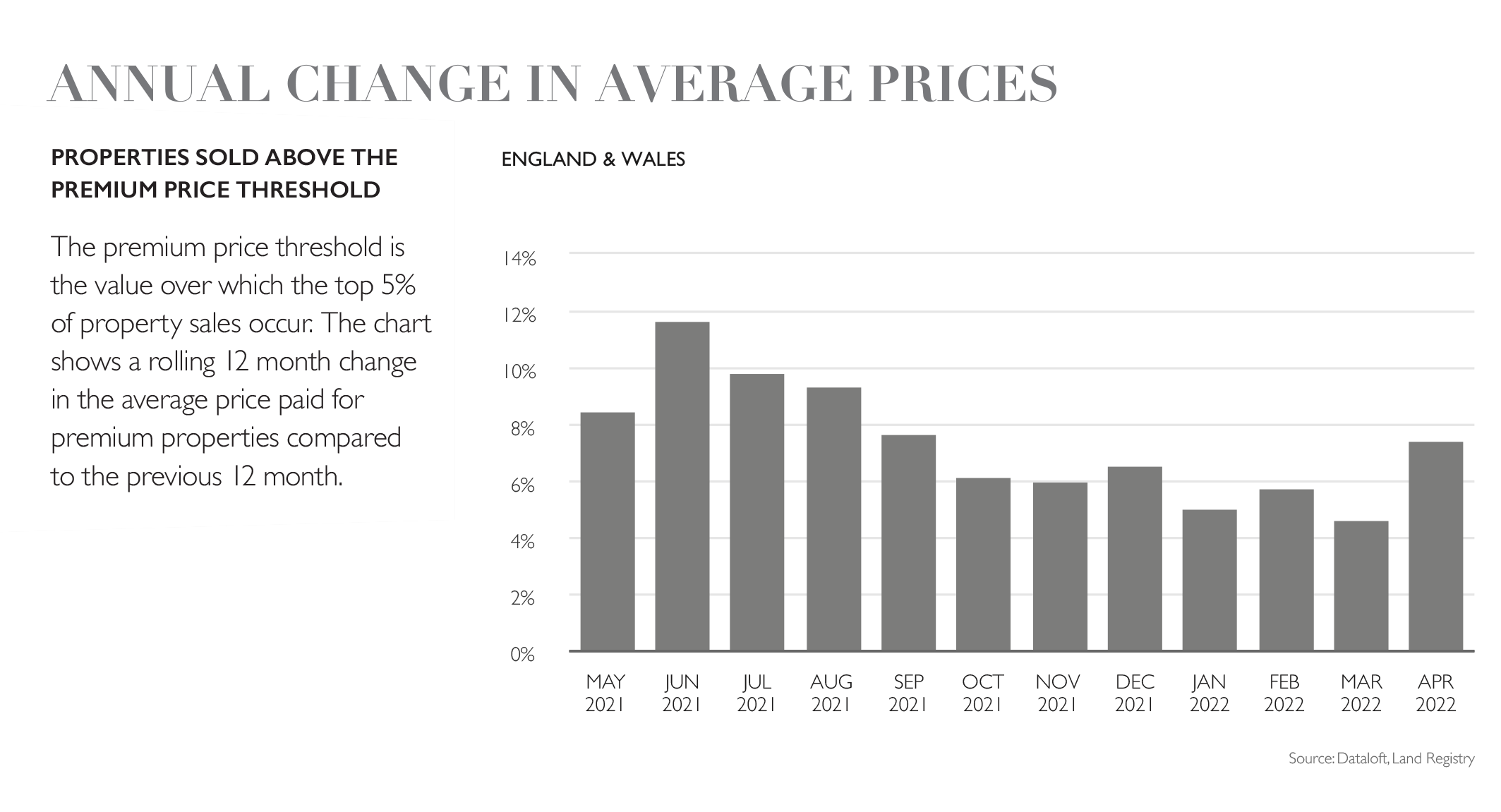

Over £14 billion was collected in residential stamp duty receipts across England and Wales in the year to March 2022, up 18% on the pre-pandemic year April 2019-March 2020 (HMRC, StatsWales). More than 33,000 sales priced £1 million or more took place in the year to March 2022, up 68% on the pre-pandemic year. While property price growth will have pushed sales into higher tax brackets, it is clear that interest in the prime markets continues. These markets are forecast to outperform the mainstream markets over the next five years as wealthier buyers are, in the main, less impacted by interest rate rises and the cost-of-living crisis. At 7.4%, annual price growth in the prime markets of England and Wales has risen to its strongest level of growth since September and the premium price threshold for a prime market property has broken the £800,000 barrier.

Contact us

Market your home in time for spring. Get in touch with your local Fine & Country agent to sell your home today.

8th Jun 2022

More from Fine & Country

DISCOVER MORE ABOUT FINE & COUNTRY

NATIONAL MARKET REPORTS

Looking at selling, buying, investing or just interested in the prime property market? Read our latest edition of the National Housing Market Update.

Discover more »

SELLING YOUR PROPERTY

Selling your home is one of the most important decisions you make; your home is both a financial and emotional investment. Find out how we can help »

TAKE THEIR WORD FOR IT

An overwhelming majority of those who had used Fine & Country would recommend our services to a family member or friend, according to our most recent survey taken by members of the public.

To achieve 99.48% positive feedback is a privilege and we will endeavour to maintain this result. We are dedicated to offering the best possible services to every customer, whether buyer or seller, from beginning to end.

INDEPENDENT EXPERTISE

Every Fine & Country agent is a highly proficient and professional independent estate agent, operating to strict codes of conduct and dedicated to you. They will assist, advise and inform you through each stage of the property transaction.

GLOBAL EXPOSURE

With offices in over 300 locations worldwide we combine the widespread exposure of the international marketplace with national marketing campaigns and local expertise and knowledge of carefully selected independent property professionals.

UNIQUE MARKETING APPROACH

People buy as much into lifestyle of a property and its location as they do the bricks and mortar. We utilize sophisticated, intelligent and creative marketing that provides the type of information buyers would never normally see with other agents.

PARK LANE OFFICE

Access the lucrative London and international investor market from our prestigious Park Lane showrooms at 121 Park Lane, Mayfair. Our showrooms in London are amongst the very best placed in Europe, attracting clients from all over the world.

MULTI-AWARD WINNING

Our consistent efforts to offer innovative marketing combined with a high level of service have been recognised by the industry for an astounding fifth year in a row, winning Best International Real Estate Agency Marketing at the International Residential Property Awards.

4.85 out of 5 - based on 1986 customer reviews

OVER 300 LOCATIONS WORLDWIDE

Our International Network

Connecting offices on over 300 locations worldwide, our referral system combines local knowledge and expertise with an international network to find the right buyer for you wherever they are, at the same time as finding you your ideal next move

Our International Websites

SOCIAL MEDIA

We interact with customers on the main social media channels including Facebook, Twitter, YouTube, LinkedIn and Pinterest, giving each property maximum online exposure.

FINE & COUNTRY SERVICES

FINE & COUNTRY

INTERIOR DESIGN

Access Fine & Country Interior Design to put your property ahead and make it stand out. With expert advice from some of London’s best stylists and designers we will make sure it makes a statement. Or if you’re purchasing with us, let F&C ID help make your new house feel like home by helping you find the very best specialists and designers for property refurbishment. Find out more »

FINE & COUNTRY

FOREIGN EXCHANGE

We have partnered with Rational FX, one of the world’s leading foreign exchange specialists to provide private and tailored currency services for all of our clients buying and selling luxury property around the world. Find out how we can help »

BUYING AGENT SERVICE

We understand that your time is precious, so save the time, money and stress of searching for a property with a buying agent. Also giving you access to off-market and discreetly marketed properties.

MEDIA CENTRE

Our internal Media Centre is a team of experienced press relations managers and copy writers dedicated to liaising with newspapers, magazines and other media outlets to gain extensive coverage for our properties in national and local media.

FINE & COUNTRY PUBLICATIONS

{kind=link}

THE FINE & COUNTRY FOUNDATION

The Fine & Country Foundation is dedicated to supporting and funding homeless causes in the UK and overseas. Fine & Country offices organise a range of fundraising events for you to get involved in and/ or support. Find out more about our work here. Read more »

*Please, note: for security reasons, the maps on this website do not provide the exact location of the property and they are provided solely as an indication of area.